Navigate the upcoming changes in Medicare Part B premiums for 2025. Knowing these details is essential for smart financial planning and optimal healthcare coverage.

Understanding Medicare Part B

Medicare Part B is a critical component of the United States healthcare system for seniors and certain younger individuals with disabilities. It primarily covers outpatient medical services, including doctor visits, preventive services, durable medical equipment, and some types of home health care. Unlike Medicare Part A, which covers inpatient hospital stays, Part B is designed to ensure that beneficiaries have access to necessary and routine medical care without the burden of exorbitant out-of-pocket costs.

One of the essential aspects of Medicare Part B is its focus on preventive services. This includes screenings for conditions such as cancer, diabetes, and cardiovascular disease, as well as vaccinations and wellness visits. These preventive measures are invaluable in detecting potential health issues early, thereby reducing the need for more intensive and costly treatments down the line. By prioritizing early detection and prevention, Medicare Part B helps to improve the overall health outcomes for its beneficiaries.

Understanding how Medicare Part B works is crucial for those who are or will be eligible for Medicare. This includes knowing what is covered under Part B, how much it costs, and how to enroll. It’s also important to be aware of the changes that can occur from year to year, particularly with respect to premiums. By staying informed, beneficiaries can make better decisions about their healthcare and financial planning.

Overview of Medicare Part B Premiums

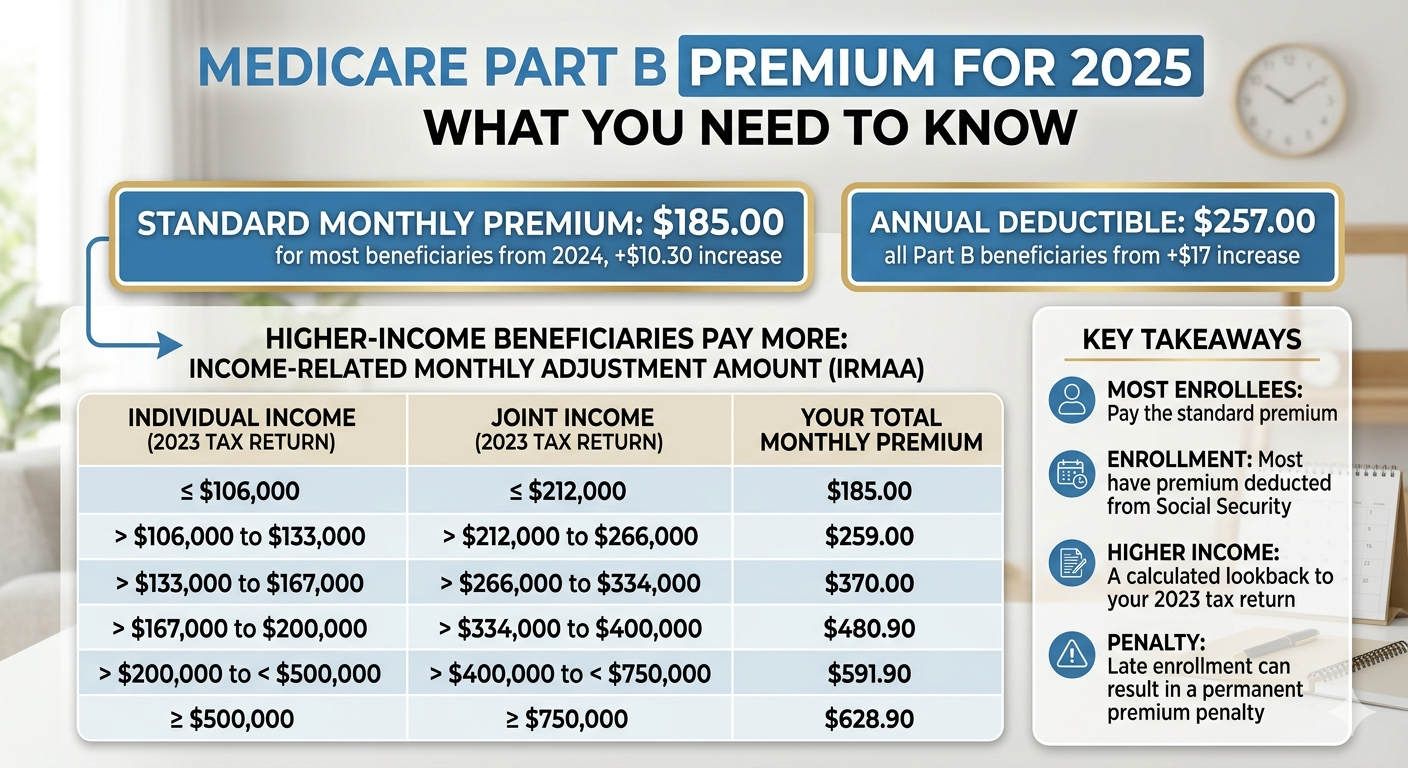

Medicare Part B premiums are the monthly payments that beneficiaries must make to maintain their coverage. These premiums are set annually by the Centers for Medicare & Medicaid Services (CMS) and can vary based on a number of factors, including income. The standard premium amount is typically announced in the fall for the upcoming year, giving beneficiaries time to adjust their budgets accordingly.

For most beneficiaries, the standard premium amount is automatically deducted from their Social Security benefits. However, those who do not receive Social Security benefits will need to make arrangements to pay their premiums directly. In addition to the standard premium, some individuals may be subject to additional charges based on their income, known as the Income-Related Monthly Adjustment Amount (IRMAA). This can significantly increase the overall cost of Medicare Part B coverage.

It’s important to note that while the standard premium amount is the same for most beneficiaries, there can be variations based on when an individual enrolls in Medicare Part B. For example, those who delay enrollment without having other credible coverage may face a late enrollment penalty, which is an additional charge added to their monthly premium. Understanding these nuances can help beneficiaries avoid unexpected costs and ensure they maintain continuous coverage.

Projected Changes for 2025

As we look ahead to 2025, there are several projected changes to Medicare Part B premiums that beneficiaries should be aware of. These changes are influenced by various factors, including healthcare inflation, legislative adjustments, and the overall financial health of the Medicare program. While the exact premium amounts for 2025 have not yet been finalized, early projections indicate that there may be a modest increase compared to previous years.

One of the primary drivers of premium changes is the overall cost of healthcare services. As medical costs continue to rise, so too do the expenses associated with providing coverage. This includes not only the cost of medical services themselves but also administrative expenses and other overheads. As a result, beneficiaries can expect to see a corresponding increase in their Part B premiums to help cover these costs.

Another factor that could impact premiums in 2025 is potential legislative changes. Congress periodically reviews and adjusts Medicare funding and policies, which can have a direct impact on premiums. For example, proposals to expand coverage or introduce new benefits could lead to higher costs, while efforts to reduce waste and improve efficiency could help to keep premiums more stable. Staying informed about these potential changes can help beneficiaries better plan for their future healthcare expenses.

Factors Influencing Premium Rates

Several factors influence the rates of Medicare Part B premiums, making it essential for beneficiaries to understand what drives these costs. One of the primary factors is the overall economic environment, including inflation rates and the general cost of living. As healthcare costs rise, so too do the expenses associated with providing Medicare coverage, which can lead to higher premiums.

Another critical factor is the utilization of healthcare services by beneficiaries. When more people use medical services, the overall cost of providing coverage increases. This can be influenced by demographic trends, such as an aging population or an increase in the prevalence of chronic conditions. Higher utilization rates can put additional strain on the Medicare program, necessitating adjustments to premiums to ensure the program remains financially sustainable.

Policy changes and legislative actions also play a significant role in determining premium rates. For instance, changes to Medicare reimbursement rates for healthcare providers, adjustments to the benefits covered under Part B, and initiatives to improve efficiency and reduce waste can all impact premium amounts. Additionally, broader healthcare reforms at the federal level can have ripple effects on the Medicare program, influencing both the costs and the structure of premiums.

The Income-Related Monthly Adjustment Amount (IRMAA)

The Income-Related Monthly Adjustment Amount (IRMAA) is an additional charge that applies to Medicare Part B premiums for beneficiaries with higher incomes. This adjustment is designed to ensure that those who have greater financial resources contribute more to the cost of their healthcare coverage. IRMAA is determined based on an individual’s modified adjusted gross income (MAGI) as reported on their tax return from two years prior.

For 2025, the specific income thresholds and corresponding IRMAA amounts will be announced closer to the start of the year. However, it’s important for beneficiaries to be aware of how IRMAA works and how it might affect their premiums. Generally, the higher a beneficiary’s income, the higher their IRMAA will be. This can result in significantly higher monthly premiums for those in the top income brackets.

Beneficiaries who are subject to IRMAA will receive a notice from the Social Security Administration informing them of their adjusted premium amount. It’s possible to appeal the IRMAA determination if a beneficiary’s income has decreased due to a life-changing event, such as retirement, divorce, or the death of a spouse. Understanding the IRMAA process and knowing how to navigate it can help beneficiaries manage their healthcare costs more effectively.

How to Pay Your Medicare Part B Premium

Paying your Medicare Part B premium is a straightforward process, but it’s important to understand the different methods available to ensure timely and accurate payments. For most beneficiaries, the standard premium amount is automatically deducted from their Social Security benefits, making it a seamless and hassle-free process. However, for those who do not receive Social Security benefits, alternative payment methods are available.

One option is to set up automatic payments through your bank or financial institution. This can be done by setting up a recurring payment to the Centers for Medicare & Medicaid Services (CMS) to ensure your premium is paid on time each month. Another option is to use Medicare Easy Pay, a free service that allows you to have your premium automatically deducted from your checking or savings account each month.

For those who prefer to pay their premiums manually, it’s possible to make payments by mail using a check or money order. CMS provides detailed instructions on where to send your payment and what information to include to ensure it is processed correctly. Regardless of the payment method you choose, it’s important to keep track of your payments and ensure they are made on time to avoid any interruptions in your coverage.

Enrollment Periods and Deadlines

Understanding the enrollment periods and deadlines for Medicare Part B is crucial for ensuring continuous coverage and avoiding late enrollment penalties. The Initial Enrollment Period (IEP) is the first opportunity for most individuals to enroll in Medicare Part B. This seven-month window begins three months before the month you turn 65, includes your birthday month, and extends three months after.

If you miss your IEP, you may have to wait until the General Enrollment Period (GEP) to sign up for Medicare Part B. The GEP runs from January 1 to March 31 each year, with coverage starting on July 1. However, enrolling during the GEP can result in a late enrollment penalty, which is an additional 10% of the standard premium for every 12 months you were eligible but did not enroll.

There is also a Special Enrollment Period (SEP) for individuals who are still working and have health coverage through their employer or their spouse’s employer. If you qualify for an SEP, you can enroll in Medicare Part B without penalty once your employment or employer coverage ends. Understanding these enrollment periods and planning accordingly can help you avoid unnecessary costs and ensure you have the coverage you need when you need it.

Comparing Medicare Part B with Other Parts of Medicare

Medicare is divided into four main parts, each covering different aspects of healthcare. Medicare Part B, as discussed, focuses on outpatient services and preventive care. In contrast, Medicare Part A covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care services. Understanding the differences between these parts is essential for comprehensive healthcare planning.

Medicare Part C, also known as Medicare Advantage, is an alternative to Original Medicare (Parts A and B) that allows beneficiaries to receive their benefits through private insurance plans. These plans often include additional benefits, such as dental, vision, and prescription drug coverage, which are not covered by Original Medicare. Medicare Advantage plans can offer more comprehensive coverage, but they may also come with different costs and restrictions compared to Original Medicare.

Finally, Medicare Part D covers prescription drugs. This part of Medicare is also offered through private insurance companies and helps beneficiaries manage the cost of their medications. Each part of Medicare plays a crucial role in providing comprehensive healthcare coverage, and understanding how they work together can help beneficiaries make informed decisions about their healthcare options.

Common Questions About Medicare Part B Premiums

Many beneficiaries have questions about Medicare Part B premiums, and understanding the answers can help alleviate concerns and improve decision-making. One common question is whether premiums are tax-deductible. In some cases, Medicare Part B premiums can be deducted as a medical expense on your federal income tax return if you itemize your deductions and your total medical expenses exceed 7.5% of your adjusted gross income.

Another frequently asked question is how premium amounts are determined. As mentioned earlier, premiums are set annually by the Centers for Medicare & Medicaid Services (CMS) based on factors such as healthcare costs and legislative changes. For those with higher incomes, the Income-Related Monthly Adjustment Amount (IRMAA) can also affect the total premium amount.

Beneficiaries often wonder what happens if they can’t afford their Medicare Part B premiums. There are programs available to help, such as the Medicare Savings Programs (MSPs), which assist low-income individuals with paying their premiums, deductibles, and other out-of-pocket costs. Understanding these programs and how to apply for them can provide much-needed financial relief for those struggling to afford their healthcare coverage.

Conclusion: Preparing for Your Medicare Part B Premium in 2025

As we approach 2025, staying informed about changes to Medicare Part B premiums is crucial for effective financial planning and healthcare management. Understanding the factors that influence premium rates, such as healthcare costs, legislative changes, and income adjustments, can help beneficiaries anticipate and prepare for potential increases.

By familiarizing yourself with the enrollment periods and deadlines, you can avoid costly penalties and ensure continuous coverage. Additionally, exploring payment options and assistance programs can help you manage your premiums and maintain your financial stability. Comparing Medicare Part B with other parts of Medicare can also provide a comprehensive view of your healthcare options and help you make informed decisions.

Ultimately, staying proactive and informed about your Medicare Part B premiums will enable you to navigate the complexities of the healthcare system with confidence. By taking the time to understand how premiums are determined, exploring available resources, and planning, you can ensure that you have the coverage you need to maintain your health and well-being in 2025 and beyond.

Craig Smith

Independent Medicare Insurance Broker | AHIP Certified

Craig Smith is the founder of Craig Smith Insurance Group, an independent Medicare brokerage serving seniors across New York, New Jersey, and nationwide since 2013. With over 25 years of financial services experience and 317+ five-star Google reviews, Craig helps clients compare Medicare Advantage, Medicare Supplement, and Part D plans — always free of charge.

Learn more about Craig →