One of the most important and most misunderstood aspects of Medicare is knowing when to enroll. Miss the wrong deadline, and you could face permanent premium penalties that follow you for the rest of your life. As an independent Medicare insurance broker serving clients across New York, New Jersey, and nationwide, I help people navigate Medicare enrollment every single day. Here is a clear, complete guide to every Medicare enrollment period you need to know.

If you’re turning 65 soon and want a complete overview of all your Medicare options, read our Turning 65 in New York Medicare Guide.

Why Medicare Enrollment Periods Matter

Unlike most insurance, Medicare has specific enrollment windows, and missing them can have serious financial consequences. Late enrollment penalties for Medicare Part B and Medicare Part D are permanent, meaning they increase your premiums for as long as you have Medicare. Understanding which enrollment period applies to your situation is critical to avoiding these costly mistakes.

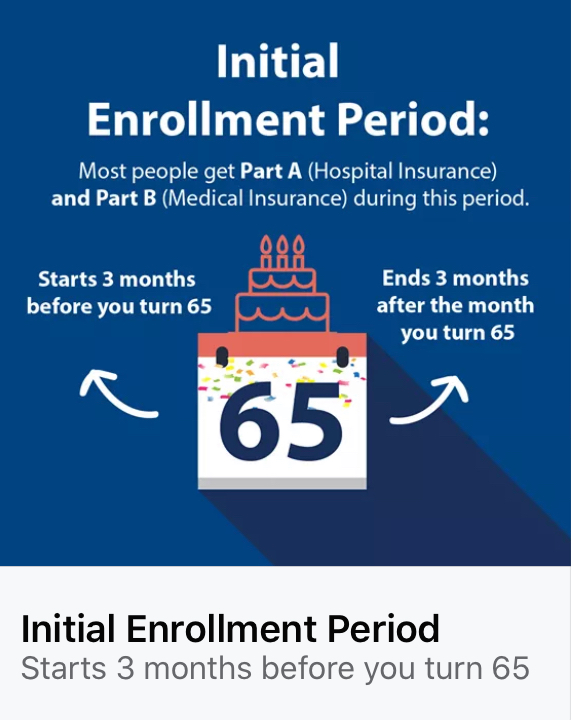

Initial Enrollment Period (IEP)

The Initial Enrollment Period is your first opportunity to enroll in Medicare. It is a 7-month window that surrounds your 65th birthday:

- 3 months before your 65th birthday month

- Your 65th birthday month

- 3 months after your 65th birthday month

When Coverage Starts During Your IEP

The timing of when your coverage begins depends on when you enroll during your IEP:

- Enroll 1–3 months before your birthday month: Coverage begins the 1st of your birthday month

- Enroll during your birthday month: Coverage begins the following month

- Enroll 1–3 months after your birthday month: Coverage begins 2–3 months after you enroll

This is why I always recommend enrolling 3 months before your 65th birthday; it ensures your coverage starts on time with no gaps.

What You Can Enroll In During Your IEP

- Medicare Part A — hospital coverage

- Medicare Part B — outpatient medical coverage

- Medicare Advantage — all-in-one alternative to Original Medicare

- Medicare Part D — prescription drug coverage

- Medicare Supplement (Medigap) — during your IEP, you have guaranteed issue rights, meaning carriers cannot deny you or charge more based on health history

General Enrollment Period (GEP)

If you missed your Initial Enrollment Period and do not qualify for a Special Enrollment Period, you can sign up during the General Enrollment Period:

- When: January 1 – March 31 each year

- Coverage begins: July 1 of that year

- Penalty: You may face a late enrollment penalty for Part B and Part D

The Part B late enrollment penalty is 10% of the standard premium for each full 12-month period you were eligible but did not enroll. This penalty is permanent and added to your premium for as long as you have Part B.

Annual Enrollment Period (AEP)

The Annual Enrollment Period — also known as Open Enrollment is the main window each year when Medicare beneficiaries can make changes to their coverage:

- When: October 15 – December 7 each year

- Coverage begins: January 1 of the following year

What You Can Do During AEP

- Switch from Original Medicare to a Medicare Advantage plan

- Switch from Medicare Advantage back to Original Medicare

- Switch from one Medicare Advantage plan to another

- Join, switch, or drop a Medicare Part D plan

AEP is the busiest time of year for Medicare brokers and for good reason. Plan benefits, premiums, and formularies change every year, so reviewing your coverage annually during AEP is strongly recommended even if you are happy with your current plan.

Medicare Advantage Open Enrollment Period (OEP)

The Medicare Advantage Open Enrollment Period gives Medicare Advantage enrollees a second chance to make changes early in the year:

- When: January 1 – March 31 each year

- Coverage begins: First day of the month after you make the change

What You Can Do During OEP

- Switch from one Medicare Advantage plan to another

- Switch from Medicare Advantage back to Original Medicare

- Join a Medicare Part D plan if you return to Original Medicare

Note: You cannot use OEP to switch from Original Medicare to Medicare Advantage; that can only be done during AEP or a Special Enrollment Period.

Special Enrollment Period (SEP)

A Special Enrollment Period allows you to enroll in or change Medicare coverage outside of the standard enrollment windows if you experience a qualifying life event. Common qualifying events include:

- Losing employer-sponsored health coverage — you have 8 months to enroll in Medicare Part B after losing coverage

- Moving to a new area not covered by your current plan

- Your plan for leaving Medicare or stopping coverage in your area

- Qualifying for Extra Help (Low-Income Subsidy) for Part D

- Moving into or out of a nursing home or other care facility

- Losing Medicaid eligibility

Important SEP Note for Working Seniors

If you are still working at 65 and covered by employer-sponsored health insurance from an employer with 20 or more employees, you can delay Medicare Part B without penalty. When you eventually retire or lose that coverage, you will have an 8-month SEP to enroll in Part B without facing a late enrollment penalty.

However, if your employer has fewer than 20 employees, Medicare becomes your primary coverage at 65, and you should enroll in Part B on time to avoid gaps and penalties.

For a complete breakdown of every qualifying life event and how each SEP works, see our Medicare Special Enrollment Periods guide.

Medigap Open Enrollment Period

The Medigap Open Enrollment Period is a separate and critically important enrollment window specifically for Medicare Supplement plans:

- When: Begins the month you turn 65 AND are enrolled in Part B — lasts 6 months

- Key benefit: During this window, you have guaranteed issue rights, and insurance companies cannot deny your application or charge higher premiums based on your health history

Once this 6-month window closes, Medigap insurers in most states can use medical underwriting, meaning they can deny coverage or charge more based on pre-existing conditions. New York is an exception; it has guaranteed-issue protections year-round, a significant advantage for New York seniors.

Medicare Enrollment Period Summary

| Enrollment Period | When | Who It’s For |

|---|---|---|

| Initial Enrollment Period (IEP) | 7 months around your 65th birthday | Everyone turning 65 |

| General Enrollment Period (GEP) | January 1 – March 31 | Those who missed the IEP |

| Annual Enrollment Period (AEP) | October 15 – December 7 | All Medicare beneficiaries |

| Medicare Advantage OEP | January 1 – March 31 | Medicare Advantage enrollees |

| Special Enrollment Period (SEP) | Triggered by a qualifying event | Those with qualifying life events |

| Medigap Open Enrollment | 6 months starting at 65 with Part B | New Medicare enrollees |

One of the most important and most misunderstood aspects of Medicare is knowing when to enroll. Miss the wrong deadline, and you could face permanent premium penalties that follow you for the rest of your life. As an independent Medicare insurance broker serving clients across New York, New Jersey, and nationwide, I help people navigate Medicare enrollment every single day. Here is a clear, complete guide to every Medicare enrollment period you need to know.

If you’re turning 65 soon and want a complete overview of all your Medicare options, read our Turning 65 in New York Medicare Guide.

Why Medicare Enrollment Periods Matter

Unlike most insurance, Medicare has specific enrollment windows, and missing them can have serious financial consequences. Late enrollment penalties for Medicare Part B and Medicare Part D are permanent — meaning they increase your premiums for as long as you have Medicare. Understanding which enrollment period applies to your situation is critical to avoiding these costly mistakes.

Initial Enrollment Period (IEP)

The Initial Enrollment Period is your first opportunity to enroll in Medicare. It is a 7-month window that surrounds your 65th birthday:

- 3 months before your 65th birthday month

- Your 65th birthday month

- 3 months after your 65th birthday month

When Coverage Starts During Your IEP

The timing of when your coverage begins depends on when you enroll during your IEP:

- Enroll 1–3 months before your birthday month: Coverage begins the 1st of your birthday month

- Enroll during your birthday month: Coverage begins the following month

- Enroll 1–3 months after your birthday month: Coverage begins 2–3 months after you enroll

This is why I always recommend enrolling 3 months before your 65th birthday; it ensures your coverage starts on time with no gaps.

What You Can Enroll In During Your IEP

- Medicare Part A — hospital coverage

- Medicare Part B — outpatient medical coverage

- Medicare Advantage — all-in-one alternative to Original Medicare

- Medicare Part D — prescription drug coverage

- Medicare Supplement (Medigap) — during your IEP, you have guaranteed issue rights, meaning carriers cannot deny you or charge more based on health history

General Enrollment Period (GEP)

If you missed your Initial Enrollment Period and do not qualify for a Special Enrollment Period, you can sign up during the General Enrollment Period:

- When: January 1 – March 31 each year

- Coverage begins: July 1 of that year

- Penalty: You may face a late enrollment penalty for Part B and Part D

The Part B late enrollment penalty is 10% of the standard premium for each full 12-month period you were eligible but did not enroll. This penalty is permanent and added to your premium for as long as you have Part B.

Annual Enrollment Period (AEP)

The Annual Enrollment Period — also known as Open Enrollment is the main window each year when Medicare beneficiaries can make changes to their coverage:

- When: October 15 – December 7 each year

- Coverage begins: January 1 of the following year

What You Can Do During AEP

- Switch from Original Medicare to a Medicare Advantage plan

- Switch from Medicare Advantage back to Original Medicare

- Switch from one Medicare Advantage plan to another

- Join, switch, or drop a Medicare Part D plan

AEP is the busiest time of year for Medicare brokers — and for good reason. Plan benefits, premiums, and formularies change every year, so reviewing your coverage annually during AEP is strongly recommended even if you are happy with your current plan.

Worried that recent Medicare Advantage changes could affect your coverage? See our breakdown of whether Medicare Advantage plans are going away.

Medicare Advantage Open Enrollment Period (OEP)

The Medicare Advantage Open Enrollment Period gives Medicare Advantage enrollees a second chance to make changes early in the year:

- When: January 1 – March 31 each year

- Coverage begins: First day of the month after you make the change

What You Can Do During OEP

- Switch from one Medicare Advantage plan to another

- Switch from Medicare Advantage back to Original Medicare

- Join a Medicare Part D plan if you return to Original Medicare

Note: You cannot use OEP to switch from Original Medicare to Medicare Advantage; that can only be done during AEP or a Special Enrollment Period.

Special Enrollment Period (SEP)

A Special Enrollment Period allows you to enroll in or change Medicare coverage outside of the standard enrollment windows if you experience a qualifying life event. Common qualifying events include:

- Losing employer-sponsored health coverage — you have 8 months to enroll in Medicare Part B after losing coverage

- Moving to a new area not covered by your current plan

- Your plan for leaving Medicare or stopping coverage in your area

- Qualifying for Extra Help (Low-Income Subsidy) for Part D

- Moving into or out of a nursing home or other care facility

- Losing Medicaid eligibility

Important SEP Note for Working Seniors

If you are still working at 65 and covered by employer-sponsored health insurance from an employer with 20 or more employees, you can delay Medicare Part B without penalty. When you eventually retire or lose that coverage, you will have an 8-month SEP to enroll in Part B without facing a late enrollment penalty.

However, if your employer has fewer than 20 employees, Medicare becomes your primary coverage at 65, and you should enroll in Part B on time to avoid gaps and penalties.

Medigap Open Enrollment Period

The Medigap Open Enrollment Period is a separate and critically important enrollment window specifically for Medicare Supplement plans:

- When: Begins the month you turn 65 AND are enrolled in Part B — lasts 6 months

- Key benefit: During this window, you have guaranteed issue rights, and insurance companies cannot deny your application or charge higher premiums based on your health history

Once this 6-month window closes, Medigap insurers in most states can use medical underwriting, meaning they can deny coverage or charge more based on pre-existing conditions. New York is an exception; it has guaranteed-issue protections year-round, a significant advantage for New York seniors.

Medicare Enrollment Period Summary

| Enrollment Period | When | Who It’s For |

|---|---|---|

| Initial Enrollment Period (IEP) | 7 months around your 65th birthday | Everyone turning 65 |

| General Enrollment Period (GEP) | January 1 – March 31 | Those who missed the IEP |

| Annual Enrollment Period (AEP) | October 15 – December 7 | All Medicare beneficiaries |

| Medicare Advantage OEP | January 1 – March 31 | Medicare Advantage enrollees |

| Special Enrollment Period (SEP) | Triggered by a qualifying event | Those with qualifying life events |

| Medigap Open Enrollment | 6 months starting at 65 with Part B | New Medicare enrollees |

For a complete walkthrough on how to enroll, see our step-by-step guide to applying for Medicare

Frequently Asked Questions — Medicare Enrollment Periods

What happens if I miss my Medicare Initial Enrollment Period?

If you miss your IEP without a qualifying reason, you will need to wait for the General Enrollment Period January 1 through March 31, and your coverage won’t begin until July 1. You may also face permanent late enrollment penalties for Part B and Part D.

Can I enroll in Medicare anytime during the year?

No — Medicare enrollment is limited to specific windows. The only exception is if you qualify for a Special Enrollment Period due to a qualifying life event such as losing employer coverage.

When is the best time to enroll in Medicare?

The best time is 3 months before your 65th birthday, which ensures your coverage starts on time with no gaps. I recommend contacting a Medicare broker 4 to 6 months before your 65th birthday to give yourself plenty of time to compare plans and make an informed decision.

Do I need to re-enroll in Medicare every year?

No, your Medicare coverage automatically renews each year. However, you should review your plan annually during the Annual Enrollment Period to make sure your current plan still offers the best value for your needs.

What is the difference between the Annual Enrollment Period and the Medicare Advantage Open Enrollment Period?

The Annual Enrollment Period (AEP) runs October 15 – December 7 and is open to all Medicare beneficiaries. During AEP, you can join, switch, or drop a Medicare Advantage or Part D plan. The Medicare Advantage Open Enrollment Period (OEP) runs January 1 – March 31 and is only for people already enrolled in Medicare Advantage. It lets you switch to a different Advantage plan or return to Original Medicare, but you cannot use OEP to join Medicare Advantage for the first time.

Can I be penalized for enrolling in Medicare late?

Yes, and the penalties are permanent. The Part B late enrollment penalty is 10% of the standard premium for each full 12-month period you went without coverage when you were eligible. The Part D late enrollment penalty is 1% of the national base beneficiary premium for each month you went without creditable drug coverage. Both penalties are added to your monthly premium for as long as you have Medicare.

What qualifies as a Special Enrollment Period trigger?

The most common SEP triggers are: losing employer-sponsored health insurance, moving to a new service area, your plan leaving Medicare, gaining or losing Medicaid eligibility, and qualifying for Extra Help (Low Income Subsidy) for Part D. The most important one for most people is losing employer coverage; when that happens, you have 8 months to enroll in Medicare Part B without penalty.

Does my spouse’s employer insurance count as creditable coverage to delay Medicare?

Yes, if you are covered under your spouse’s active employer plan and the employer has 20 or more employees, you can delay Medicare Part B without penalty. When that coverage ends, you’ll have an 8-month Special Enrollment Period to enroll in Part B.

Get Help Navigating Medicare Enrollment

Medicare enrollment windows are strict, and the penalties for missing them are permanent. Whether you are approaching 65, leaving employer coverage, or simply want to review your options during open enrollment, I am here to help.

As an independent Medicare broker serving clients across New York, New Jersey, and nationwide, I provide free, unbiased guidance to help you enroll in the right plan at exactly the right time.

📞 Contact Craig Smith Insurance Group today at (917) 740-1895 for your free Medicare enrollment consultation. No pressure, no obligation — just straightforward Medicare guidance from an independent broker who genuinely cares about getting you the right coverage.

Craig Smith

Independent Medicare Insurance Broker | AHIP Certified

Craig Smith is the founder of Craig Smith Insurance Group, an independent Medicare brokerage serving seniors across New York, New Jersey, and nationwide since 2013. With over 25 years of financial services experience and 317+ five-star Google reviews, Craig helps clients compare Medicare Advantage, Medicare Supplement, and Part D plans — always free of charge.

Learn more about Craig →